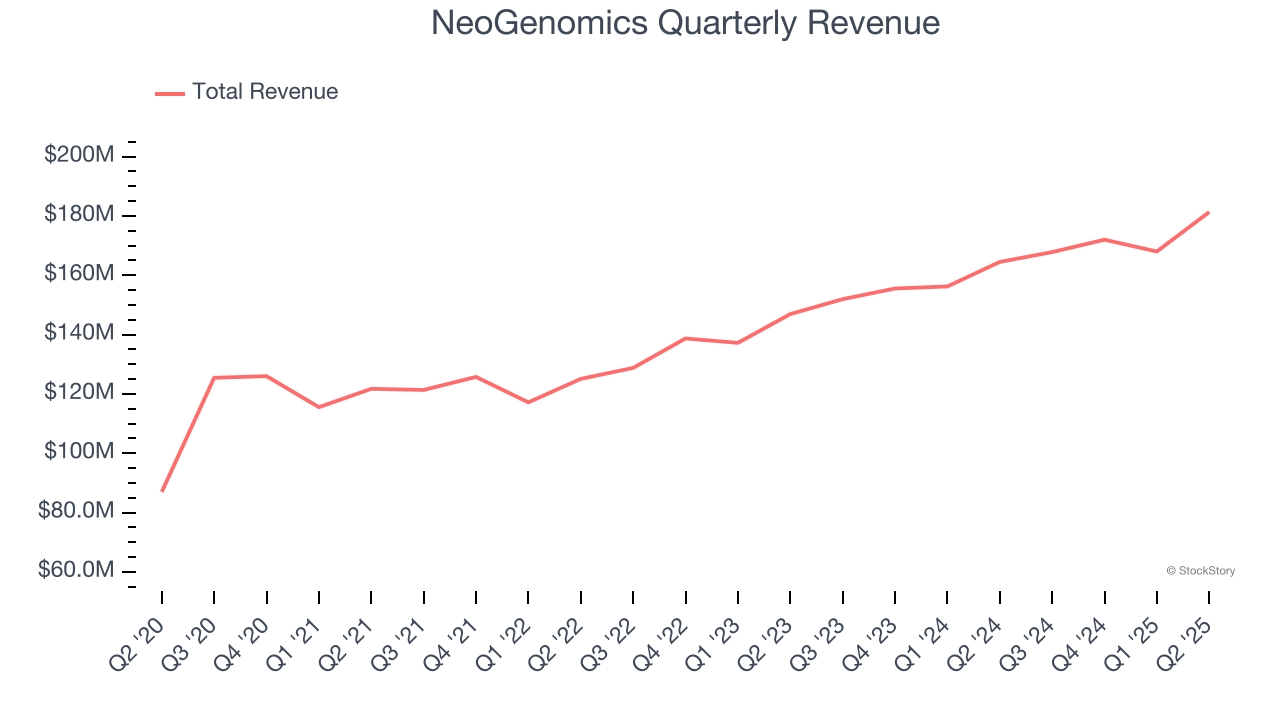

Oncology (cancer) diagnostics company NeoGenomics (NASDAQ:NEO) missed Wall Street’s revenue expectations in Q2 CY2025, but sales rose 10.2% year on year to $181.3 million. The company’s full-year revenue guidance of $723 million at the midpoint came in 2.9% below analysts’ estimates. Its non-GAAP profit of $0.03 per share was in line with analysts’ consensus estimates.

Is now the time to buy NeoGenomics? Find out by accessing our full research report, it’s free.

NeoGenomics (NEO) Q2 CY2025 Highlights:

- Revenue: $181.3 million vs analyst estimates of $182.9 million (10.2% year-on-year growth, 0.9% miss)

- Adjusted EPS: $0.03 vs analyst estimates of $0.02 (in line)

- Adjusted EBITDA: $10.68 million vs analyst estimates of $11.31 million (5.9% margin, 5.6% miss)

- The company dropped its revenue guidance for the full year to $723 million at the midpoint from $753 million, a 4% decrease

- Adjusted EPS guidance for the full year is $0.10 at the midpoint, missing analyst estimates by 36.1%

- EBITDA guidance for the full year is $42.5 million at the midpoint, below analyst estimates of $54.7 million

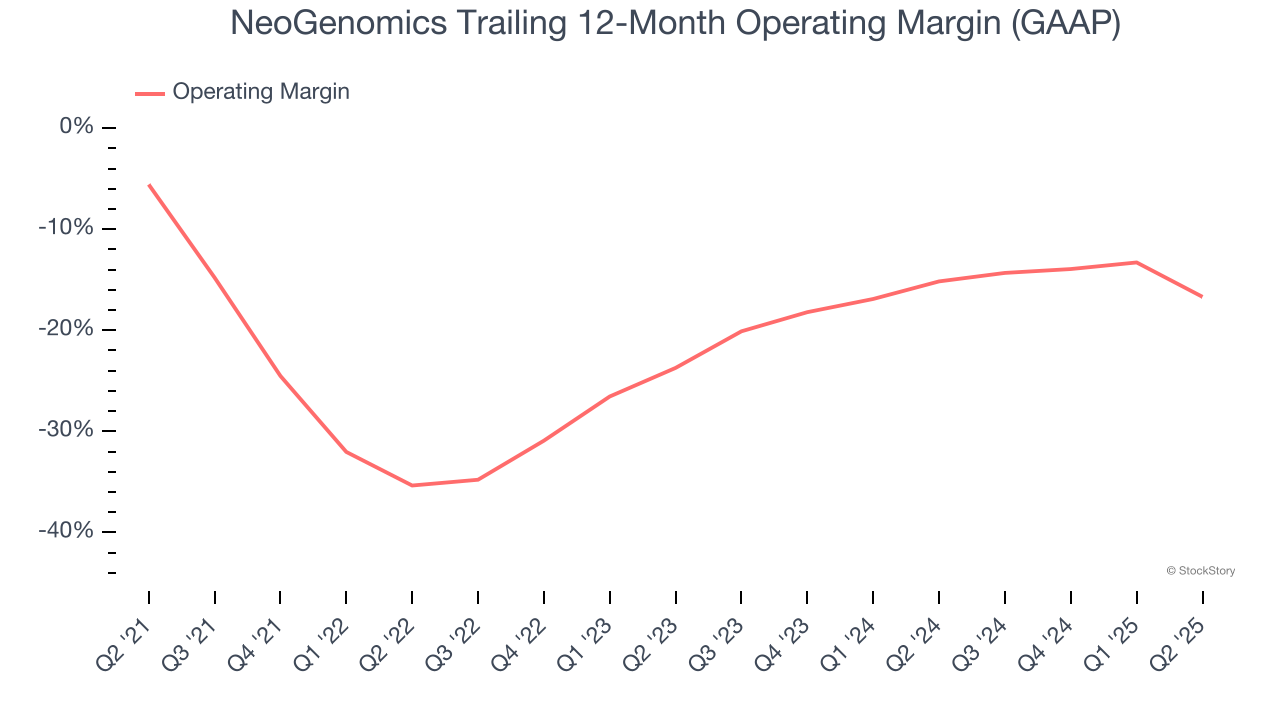

- Operating Margin: -26.3%, down from -13.3% in the same quarter last year

- Free Cash Flow Margin: 13.7%, up from 0.5% in the same quarter last year

- Market Capitalization: $831.4 million

“In the second quarter clinical revenue increased by 16% driven by sequential improvement in AUP, a record quarter for volumes, and NGS growth of 23%,” said Tony Zook, CEO of NeoGenomics.

Company Overview

Operating a network of CAP-accredited and CLIA-certified laboratories across the United States and United Kingdom, NeoGenomics (NASDAQ:NEO) provides specialized cancer diagnostic testing services, including genetic analysis, molecular testing, and pathology consultation for oncologists and healthcare providers.

Revenue Growth

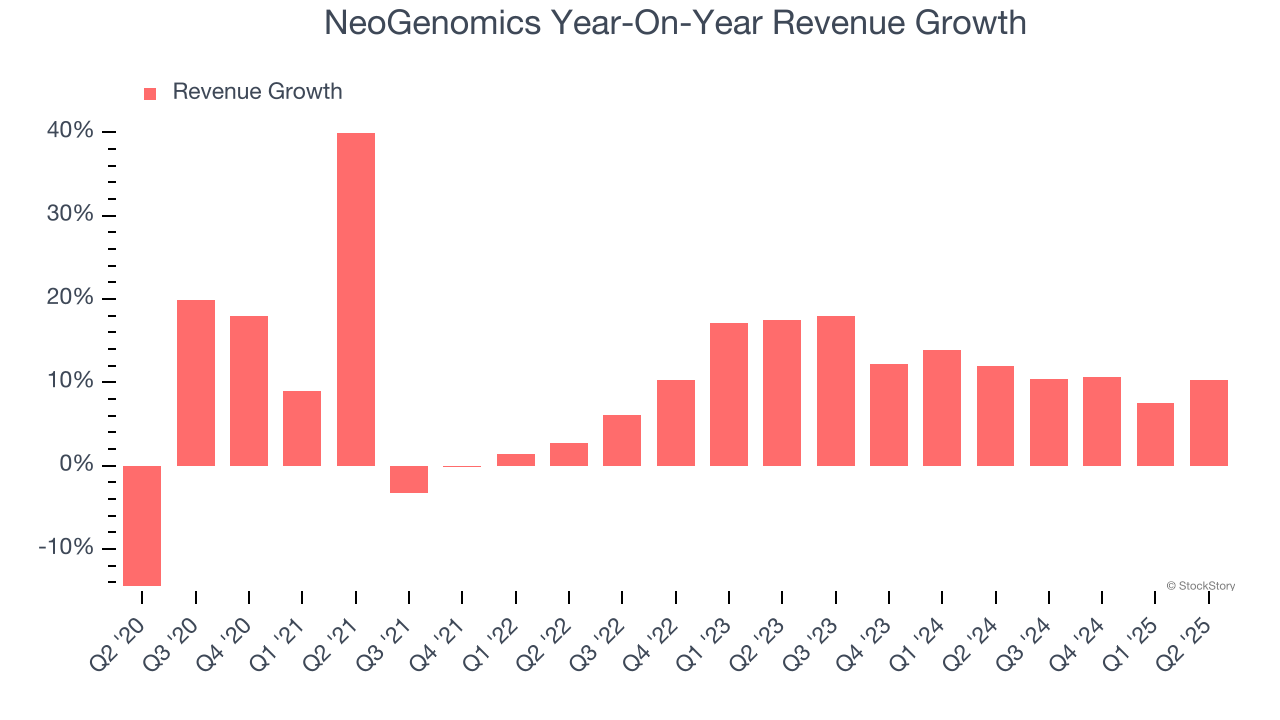

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, NeoGenomics’s sales grew at a decent 11.2% compounded annual growth rate over the last five years. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. NeoGenomics’s annualized revenue growth of 11.8% over the last two years aligns with its five-year trend, suggesting its demand was stable.

This quarter, NeoGenomics’s revenue grew by 10.2% year on year to $181.3 million but fell short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 14.4% over the next 12 months, an improvement versus the last two years. This projection is healthy and implies its newer products and services will fuel better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

NeoGenomics’s high expenses have contributed to an average operating margin of negative 19% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Looking at the trend in its profitability, NeoGenomics’s operating margin decreased by 11.1 percentage points over the last five years, but it rose by 7 percentage points on a two-year basis. Still, shareholders will want to see NeoGenomics become more profitable in the future.

In Q2, NeoGenomics generated a negative 26.3% operating margin. The company's consistent lack of profits raise a flag.

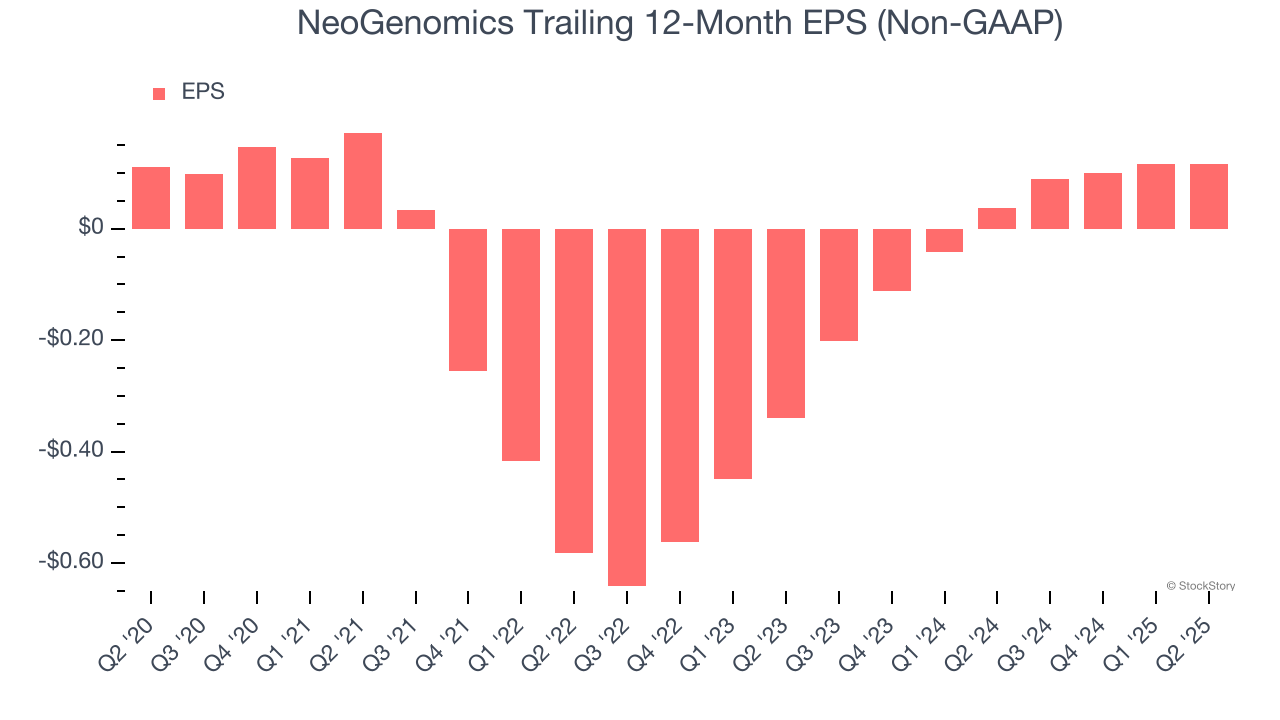

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

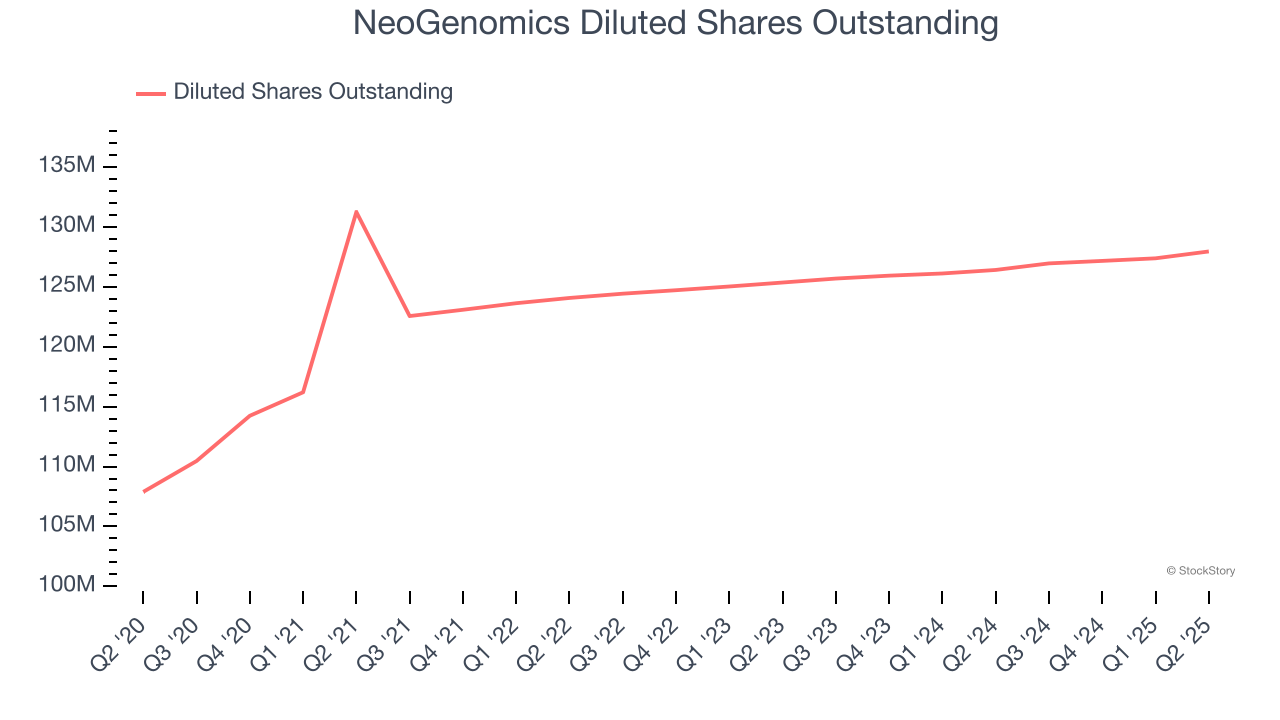

NeoGenomics’s EPS grew at an unimpressive 1.1% compounded annual growth rate over the last five years, lower than its 11.2% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Diving into the nuances of NeoGenomics’s earnings can give us a better understanding of its performance. As we mentioned earlier, NeoGenomics’s operating margin declined by 11.1 percentage points over the last five years. Its share count also grew by 18.6%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q2, NeoGenomics reported EPS at $0.03, in line with the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects NeoGenomics to perform poorly. Analysts forecast its full-year EPS of $0.12 will hit $0.24.

Key Takeaways from NeoGenomics’s Q2 Results

Revenue in the quarter missed, and the company lowered its full-year revenue guidance. Full-year EPS guidance also came in below expectations. Overall, this was a terrible quarter. The stock traded down 15.8% to $5.45 immediately following the results.

The latest quarter from NeoGenomics’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.