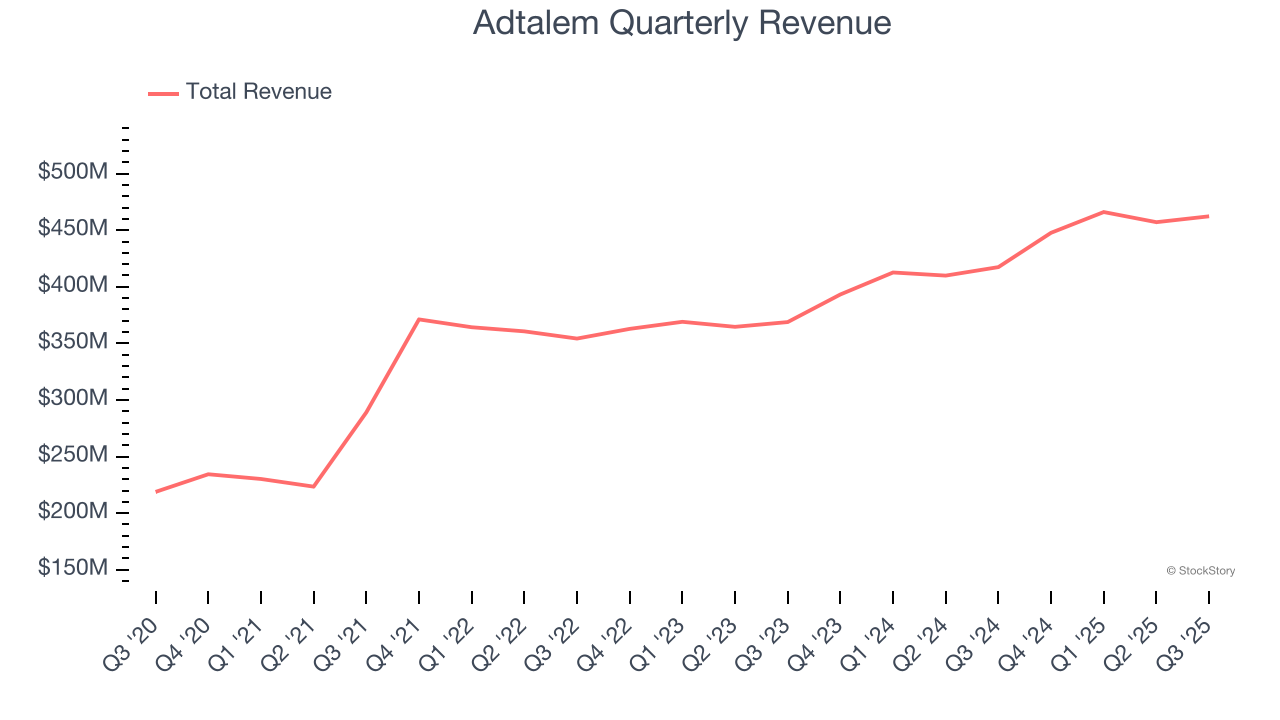

Vocational education company Adtalem Global Education (NYSE:ATGE) reported revenue ahead of Wall Streets expectations in Q3 CY2025, with sales up 10.8% year on year to $462.3 million. The company expects the full year’s revenue to be around $1.92 billion, close to analysts’ estimates. Its non-GAAP profit of $1.75 per share was 10.9% above analysts’ consensus estimates.

Is now the time to buy Adtalem? Find out by accessing our full research report, it’s free for active Edge members.

Adtalem (ATGE) Q3 CY2025 Highlights:

- Revenue: $462.3 million vs analyst estimates of $453.3 million (10.8% year-on-year growth, 2% beat)

- Adjusted EPS: $1.75 vs analyst estimates of $1.58 (10.9% beat)

- Adjusted EBITDA: $112 million vs analyst estimates of $108.3 million (24.2% margin, 3.4% beat)

- The company reconfirmed its revenue guidance for the full year of $1.92 billion at the midpoint

- Management reiterated its full-year Adjusted EPS guidance of $7.75 at the midpoint

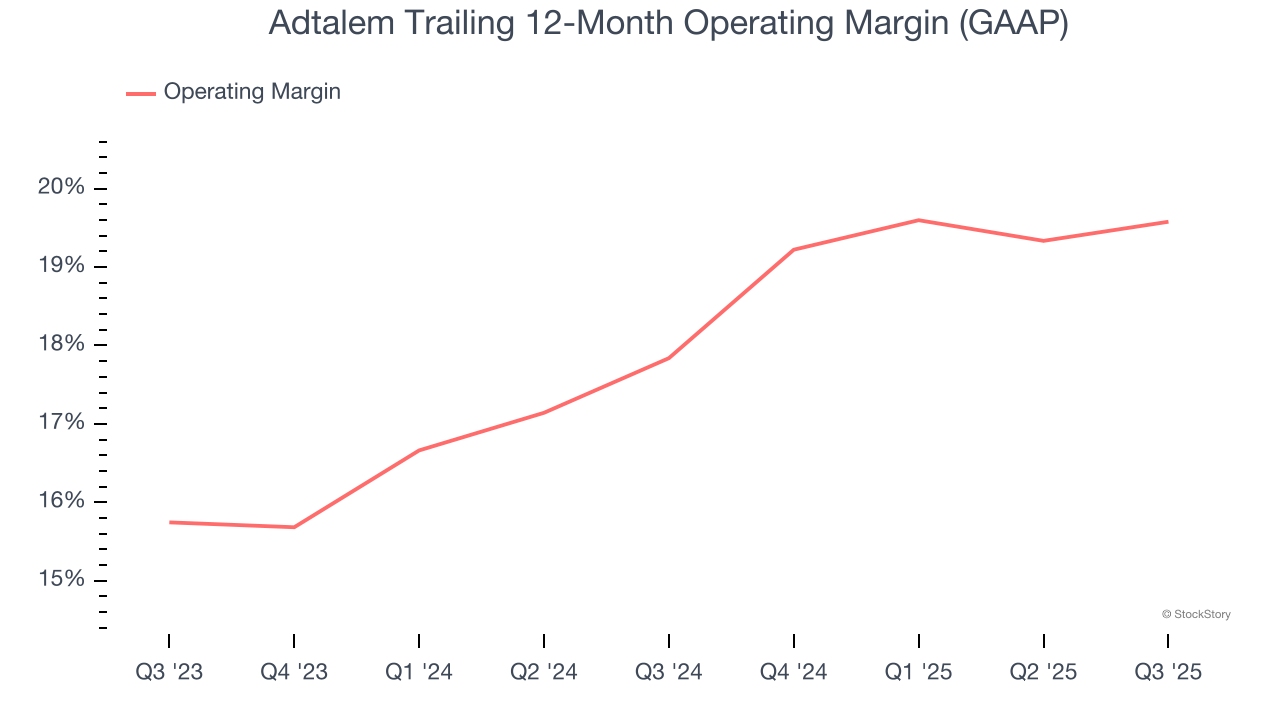

- Operating Margin: 18.5%, up from 17.3% in the same quarter last year

- Free Cash Flow Margin: 24.8%, up from 18.9% in the same quarter last year

- Market Capitalization: $5.12 billion

Company Overview

Formerly known as DeVry Education Group, Adtalem Global Education (NYSE:ATGE) is a global provider of workforce solutions and educational services.

Revenue Growth

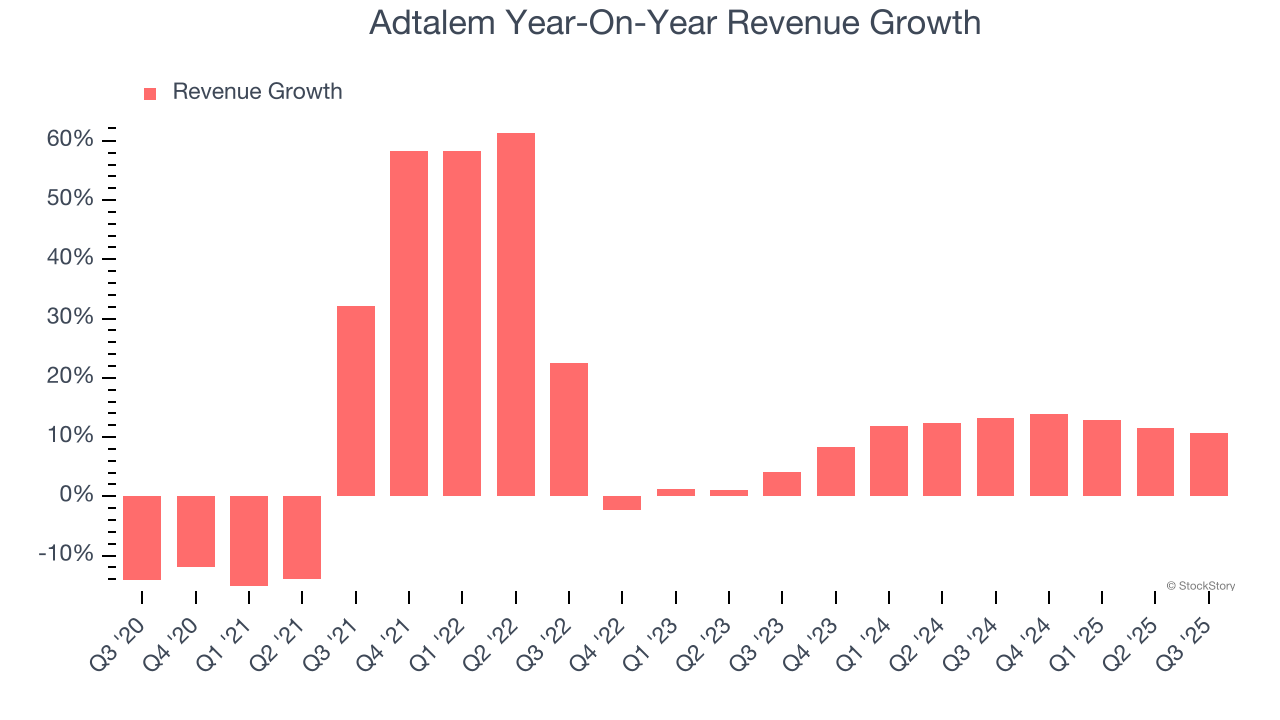

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Adtalem grew its sales at a 12.5% compounded annual growth rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the consumer discretionary sector, which enjoys a number of secular tailwinds.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Adtalem’s annualized revenue growth of 11.8% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, Adtalem reported year-on-year revenue growth of 10.8%, and its $462.3 million of revenue exceeded Wall Street’s estimates by 2%.

Looking ahead, sell-side analysts expect revenue to grow 6.4% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Adtalem’s operating margin has been trending up over the last 12 months and averaged 18.8% over the last two years. On top of that, its profitability was top-notch for a consumer discretionary business, showing it’s an well-run company with an efficient cost structure.

This quarter, Adtalem generated an operating margin profit margin of 18.5%, up 1.2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

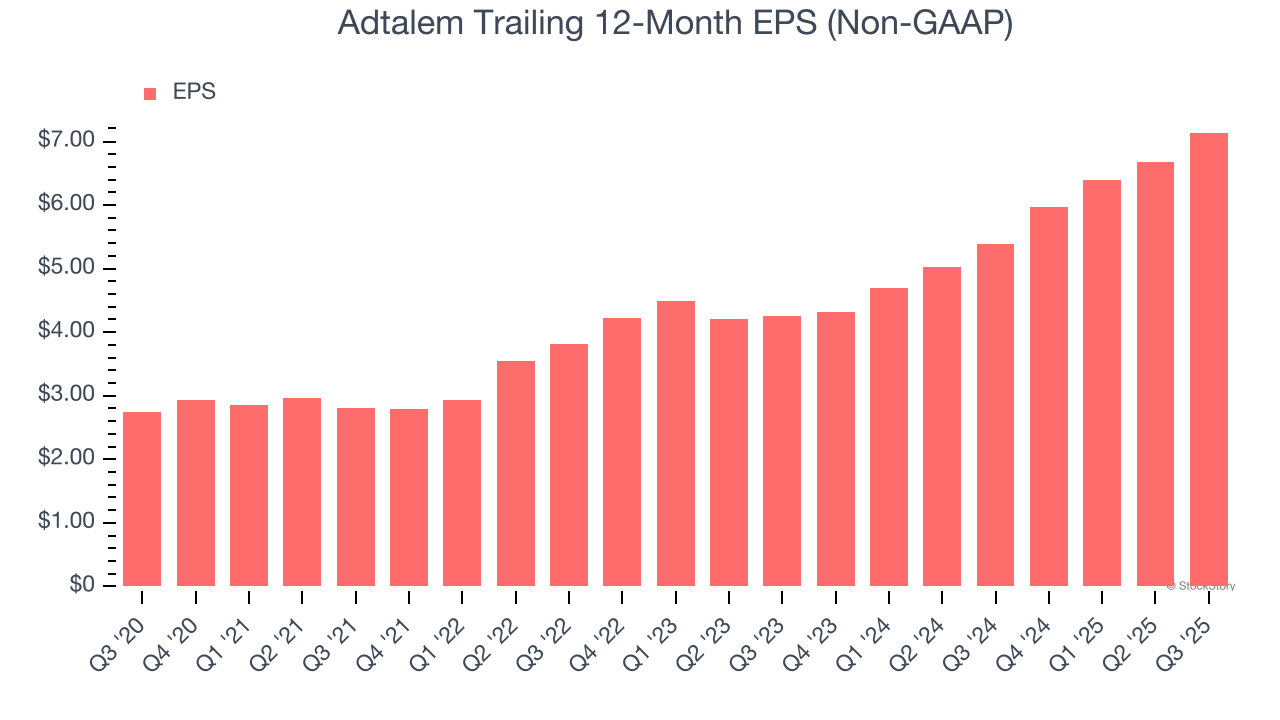

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Adtalem’s EPS grew at a spectacular 21.1% compounded annual growth rate over the last five years, higher than its 12.5% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

In Q3, Adtalem reported adjusted EPS of $1.75, up from $1.29 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Adtalem’s full-year EPS of $7.14 to grow 11.2%.

Key Takeaways from Adtalem’s Q3 Results

It was good to see Adtalem beat analysts’ EPS expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Zooming out, we think this was a decent quarter. The stock remained flat at $142.13 immediately following the results.

So should you invest in Adtalem right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.